What's Your ALE? What's Your ALE?[Thu, June 27, 2013] In a recent (February 2013) FAPIA 2013 HURRICANE SEASON TIP # 18 – Additional

Living Expense is explained for all property owners. What is it and how is it calculated? The residential insurance policy coverage

known “Additional Living Expense” (ALE) provides reimbursement for expenses that you incur as a result of a covered

peril that are over and above your normal living expenses. Business owner policies can carry "business interruption"

coverage (more on that next week). For example; Your home succumbs to fire or catastrophic hurricane damages. You have to rent a place to stay (ALE)

while your home is being re-built. You still have to pay your mortgage, But you also have to pay an additional amount of $$

to rent the place to stay (ALE) . In addition, the place you’re renting doesn’t allow pets, and you have a family

dog that nobody can take care of for you. You have to incur kennel charges (ALE) that you would not otherwise incur. You had

to stay at a hotel for 10 days (ALE) and eat out (ALE) while you were looking for a more permanent place to stay. Keep your

receipts because any amount OVER your normal food expenditure is considered ALE and is reimbursable. Finally, the catastrophic

damages in your area were so bad that you had to find a home to rent that is 50 miles away from home/work and you are incurring

additional gas and mileage expenses to travel to and from your home to check on it (ALE). Keep receipts. Some of your furniture

was not damaged but needs to be stored at a facility (ALE) during the rebuilding of your home. ALE is an “as incurred” expense

– meaning that you have to actually incur and document the expense to trigger a payment from the insurance company.

Your public adjuster can help you document these money damages to make sure you receive all the compensation you are entitled

to. Check your insurance policy today. Do you know how much ALE coverage you have? Think about having to spend an entire year

outside of your home. Do you have enough coverage to reimburse you for those additional living expenses for one year? If you

don’t, you should speak to your agent about increasing your limits. This is one of those types of coverage you don’t

want to find out you didn’t have enough of – AFTER you suffer a loss. By then, it’ll be too late. Please share this important HURRICANE SEASON

TIP brought to you by the Florida Association of Public Insurance Adjusters. If you have any questions about ALE, your property

damage or an insurance claim, please contact me.

Meteor Coverage? Really? Meteor Coverage? Really?[Wed, May 1, 2013] In a recent (February 2013) and very rare event - a meteor exploded over a city in

Russia, injuring hundreds and causing damage to buildings in six nearby cities. Local officials in the city of Chelyabinsk

estimated the damage at $32.2 million. Among the major problems – windows and walls destroyed by the shock wave from

the blast created when the meteor, which was estimated at 49 feet across, struck. While it's unlikely your home will be hit by a meteor

(I cannot recall a claim ever being filed for meteor damage), this unbelievable cosmic crash brings up the ordinary question,

what if? It is only normal to wonder. But if your home or business is insured, you should know that damage from meteors typically

would be covered under most standard policies. For instance, State Farm states that meteorites are indeed covered by most of their insurance policies. The fine print will usually list a wide range

of different damage causing perils from "fallen objects", and among

them is often a meteorite strike or explosions such as sonic blasts from meteors. Most policies are written as "open

perils", which means that they cover all events not specifically excluded in the language of the

contract. Those exclusions are usually referred to as acts of G-D and are events such as floods and earthquakes, or war and

insurrection. Under most homeowner’s policies, meteorites are covered as "falling objects".

A commercial property policy typically provides all-risk coverage that covers property damage and resulting time element loss

if there is direct physical loss or damage to insured property unless specifically excluded. Policyholders should read and question

the fine print in their individual policies first, but meteorite damage is so rare that it has not been specifically excluded

on most policies. Even if your home insurance is ambiguous, a general rule of thumb is that most policies cover damage caused

by things that fall out of the sky. Damage to property inside the building would likely be covered if the falling debris first

damages and penetrates the building roof or walls, then damages the property on the inside. Hundreds of smaller meteorites strike the

Earth’s surface every year, although only 10 to 20 are detected. Such meteorites usually reach the surface having been

burned down by the atmosphere and are too small to cause damage. What can I say, insurance companies love to cover things

that are unlikely to happen. Have questions or comments, please don't hesitate contact me. Stay safe and informed!

Our Thoughts Are With Boston Our Thoughts Are With Boston[Tue, April 16, 2013] "When evil men plot, good men must plan. When evil men burn and bomb, good men must

build and bind. When evil men shout ugly words of hatred, good men must commit themselves to the glories of love"

~Martin Luther King, Jr. The death toll in the bombings at the Boston Marathon

on a horrific afternoon of April 15th, 2013 has risen to three. Over 100 people have been injured, many of whom are in critical

condition. The horrid blast was so powerful that it blew out shop windows and damaged a window on the third floor of the Central

Library in Copley Square, which was closed to the public for Patriots’ Day. The blasts were about 50 to 100 yards apart,

reported CNN, on a stretch of the marathon course lined with spectators cheering runners through the final yards of a 26-mile,

385-yard endurance feat. My

thoughts and prayers are with the victims and their families, with the entire people of Boston, and with all the marathon

participants following these tragic events. There are no words that can fully express the grief and the grave feeling of loss. I trust that justice will be served and that evil will be defeated.

Hurricane Sandy: Ranked

As Second Costliest Storm Behind Katrina Hurricane Sandy: Ranked

As Second Costliest Storm Behind Katrina[Thu, March 28, 2013] Although headlines and news reports describing

the horror of Hurricane Sandy have ceased, many property owners

are still struggling from its aftermath. Sandy moved through 24 states, including the entire eastern seaboard from Florida to Maine

and west across the Appalachian Mountains to Michigan and Wisconsin. Sandy’s wrath effected New York and New Jersey

the most with its gale force winds and vast flooding. Many of the deaths and much of the disastrous damage in the Northeast

was caused by storm surge, which pushed water from four to nine feet above ground in New York’s Staten Island, Brooklyn

and portions of Manhattan as well as along the coast in New Jersey. As I watched in dismay the live reports and eyewitness news of Sandy’s

fury, I couldn’t help but think of all the families affected by this storm. My thoughts and heart was with the victims

and the first-response personnel. While I could not have been able to predict its utter impact, I knew what these families

would have to face once Sandy receded. Soon after the storm I and fellow Zevuloni & Associates Public Adjusters licensed in

NY, NJ and CT (among other states) were en route to the Northeast to help property owners with their insurance claims and

offer valuable information and free of charge consultations. Seeing the dreadfulness and devastation first hand was as distressing

as it was encouraging to help those affected and do all that I could to aid and assist. I am proud to say that amid the hassle

of post Sandy days, our firm sponsored a food truck feeding over 350 people in one of the worst hit neighborhoods of Brooklyn,

NY – Seagate. With doughnuts, smoothies, hot food and invaluable information station - Zevuloni & Associates were there to help! If you have been following this blog, you

know that an immediate lack of damage mitigation, overlooking key details, or failure to provide supporting evidence following

a disaster such as Hurricane Sandy could jeopardize and therefore significantly minimize a commercial or residential insurance

claim settlement. My goal was to reach out and educate property owners so that they had the proper knowledge and tools to restore

their businesses and rebuild their homes. I aspired to ensure that the insured were not cheated out of settlements which they

rightfully deserved following a massive loss. Along with a team of my co-workers, I spend many weeks which turned into months

(hence the lack of frequent blog entries since Sandy) in New York and New Jersey helping property owners to reach a maximum

and fair insurance settlement in the shortest possible period of time. Hurricane Sandy ranked among the most expensive hurricanes in history

— for both the United States and Cuba. In a recent report, the National Hurricane Center estimated damage to the

U.S. at $50 billion, the second-largest loss since 1900. Hurricane Katrina, which flooded much of New Orleans in 2005, caused

$108 billion. In Cuba, losses were estimated at $2 billion, making Sandy one of the most damaging storms ever to strike the

island.

Between $10 billion and $25 billion in losses will be covered by private insurance, according to different estimates from

risk-modeling companies that supply data to the insurance industry. The National Flood Insurance Program, which is administered by the Federal Emergency Management Agency, may incur $7.5 billion in claims

for 2012, the second-highest year after Katrina. In it’s recent reports, Tower Group Inc. (TWGP) has increased its estimated

loss from super-storm Sandy, citing higher loss-adjustment expenses on the insurer's direct business and an increase in the

amount of storm losses covered under its assumed reinsurance business and in some of its alternative investments. Tower now

projects a fourth-quarter after-tax loss from Sandy between $79 million and $81 million. The devastating consequences of Hurricane

Sandy to American families and businesses, particularly those in New York, New Jersey and Connecticut, cannot be overstated.

As those affected by the storm began the process of rebuilding and returning to normalcy, all attention has turned to their

insurance coverage and claim settlement. Please let me help you with any of your questions or concerns regarding Hurricane

Sandy claims. Don't hesitate to contact me now!

Halloween Monster: 'Frankenstorm'

Sandy Eyes East Coast [Fri, October 26, 2012]

Will Hurricane Sandy, winter

storm hybrid, dubbed "Frankenstorm" by the National Oceanic and Atmospheric Administration, ravage the U.S. East

Coast? Sandy has already claimed nearly two dozen lives in the Caribbean near

the northern Bahamas. Meteorologists warn that this hybrid storm may strike anywhere from the Delaware- Maryland-Virginia

peninsula to southern New England. The current National Hurricane Center track calls for the system to go up Delaware Bay

and almost directly over Wilmington, Delaware, just southwest of Philadelphia, on Oct. 30-31. We

urge everyone in its path to take safety precautions and prepare for impact. As always, it is better SAFE than sorry! Here

are some safety tips for hurricane preparedness: - Review and update your insurance

policy. Call your carrier, insurance agent or a licensed Public Adjuster if you have any questions about coverage and property

damage mitigation.

- Take a photo inventory of valuables in your home and office. Keep

recent purchase or repair receipts.

- Prepare a “Go Bag” and

an “Disaster Prep Kit” for all family members and pets. Assume that local pharmacies, grocery stores and gas stations

will be closed.

- Expect disruptions in electricity, gas, and water or telephone service.

- Check on friends, relatives and neighbors, especially those with

disabilities or special needs and assist them with their preparation, if possible. Coordinate and inform each other of an

evacuation disaster plan. Avoid separating your immediate family.

- Bring inside loose,

lightweight objects, such as lawn furniture, garbage cans, garden tools and toys. Anchor objects that will be unsafe to bring

inside, like gas grills or propane tanks.

- Turn off propane tanks.

- If you own a vehicle, fill your gas tank.

- If you own a boat, moor or move it

to a safe place well before the storm causes maritime conditions to deteriorate.

- If you

own a mobile home/trailer, tie it down securely.

- Shutter windows securely and brace outside

doors. Place valuables into waterproof containers or plastic bags.

- Take out extra cash and ensure that all your electrical devises are fully charged.

Here’s

what ready.gov advises you store in a disaster prep kit: - Water (one gallon per person

per day, for at least three days).

- Non-perishable food that will last at least three days, per

person.

- A battery-powered or hand-crank radio.

- A

flashlight — and extra batteries.

- A first-aid kit.

- A whistle, to signal for help.

- Dust masks, to help filter contaminated air.

- Plastic sheeting and duct tape to seal windows, doors and air vents and protect you from

debris and contaminants in the air.

- Moist towelettes.

- Garbage

bags and plastic ties.

- Wrench or pliers to turn off utilities.

- A manual can opener.

- Local maps.

- Cell phone

with chargers or solar chargers.

- Prescription medicines to last at least a week and eyeglasses

(if needed).

- Pet food.

Also, if you’re taking

care of any children, make sure to include entertainment items to keep them occupied, like games, cards, crayons and coloring

books. Review your supplies periodically to be sure you have what you need and to replace any products about to expire. You

can also buy ready-made kits for $100 or so. Keep the kit in a designated place in your home,

where it will be easy to grab if you have to scoot. And be sure all your family members know where the kit is, so any of them

can take it to a safer location. I hope that everyone will

stay safe! Wishing everyone a productive, restful and peaceful weekend!

Please keep my office number handy in case a disaster strikes and causes property damage to your home or business. The number is 877.ZEVULONI

(938.8566).

Unhappy With Your Insurance Company? You

Are Not Alone ... [Tue, October 16, 2012]

I recently came across this web page: http://www.consumeraffairs.com/insurance/home.html where property owners voice their scrupulous and rather infuriating experiences with insurance companies. Am I surprised?

Unfortunately not. The consumer affairs website offers a myriad of information on companies, products, scams, recalls and reviews written by either satisfied or disgruntled

consumers. A section of the website is devoted to reviews of property insurance providers and posts from the homeowners. It

is a candid look into the insurance industry from the eyes of the insured. Reading through the blunt reviews and criticisms of property owners across America, familiar

scenarios unfold. From underpaid claims to unresponsive insurance adjusters, unjust settlements or outright denials from the

insurance company happen more often than not. The aggravation of not getting a fair settlement to fix or rebuild a covered

loss, especially after the many years of faithfully paying rising insurance premiums – is a shared sentiment across

the board. It is sad to read

the many personal accounts of homeowners that are currently in financial distress because they did not have the tools to counter

their insurance company. Each day, numerous claims are denied or underpaid due to a technicality or an incorrect assessment

of a loss. I am vehemently

disappointed that consumers have rated top insurance carriers such as State Farm and Allstate

with merely one star out of five. Are insurance companies reading these reviews? Do they care? Well, if they cared enough

– I’d be out of work!

The topic of home owners insurance is one that often stirs a lot of frustration and anger among policy owners. Since 2005

I have been helping home owners, condo associations, businesses and corporate chains with their insurance claims. Licensed

in the states of FL, TX, GA, SC, NC, MD, CT, RI, ME I have vast experience with all types of claims such as hurricane &

tornado damage, fire & flood, vandalism and theft. The team at Zevuloni & Associates Public Adjusters and I can help you receive a fair and maximum settlement allowed by your policy. Don’t write another disappointing

review, let me help.

Good News for Florida Properties Damaged

by Isaac  [Tue, September 11, 2012] Florida Insurance Commissioner Kevin McCarty has issued

the following informational memorandum (OIR-12-05M) on August 30, 2012 with instructions on the applicability of the hurricane

deductible as it relates to property losses sustained from Hurricane Issac: [Tue, September 11, 2012] Florida Insurance Commissioner Kevin McCarty has issued

the following informational memorandum (OIR-12-05M) on August 30, 2012 with instructions on the applicability of the hurricane

deductible as it relates to property losses sustained from Hurricane Issac:

The purpose of this informational memorandum is to advise property insurers that Tropical

Storm/Hurricane Isaac was declared a hurricane by the National Hurricane Center of the National Weather Service on Tuesday,

August 28, 2012, at 11:20 A.M. CDT. Before

Tuesday, August 28, 2012, at 11:20 A.M. CDT, Tropical Storm/Hurricane Isaac was classified as a Tropical Storm. Section 627.4025(2)(a),

Florida Statutes, specifically defines hurricane coverage as coverage for loss or damage caused by the peril of windstorm

during a hurricane and furthermore (2)(b) provides Windstorm for purposes of paragraph (a) means wind, wind gusts, hail, rain,

tornadoes, or cyclones caused by or resulting from a hurricane which results in direct physical loss or damage to property.

Insurers are hereby

notified that the hurricane deductible shall not apply to property losses associated with a Tropical Storm/Hurricane Isaac

damage claim that occurred prior to Tuesday, August 28, 2012, at 11:20 A.M. CDT. For these property losses, all insurers must apply the

deductible that is unrelated to hurricane, generally referred to as the all other perils deductible or other than hurricane

deductible. An insurer that fails to apply the appropriate deductible is subject to administrative action. For a PDF copy, please visit: http://www.fslso.com/publications/press/OIR/OIR.12.05M.pdf So why and how does this affect you? Well, did you know that a typical home-owner's

insurance policy in Florida carries a higher deductible for hurricane related claims as opposed to other property damage losses.

Although unfair and devastating to many property owners, because of this higher deductible, insurance companies pay out less

on damages caused by a hurricane - forcing property owners to accept the financial burden to fully cover all repairs and restoration

costs. The good news for those Floridians hit by Tropical Storm Isaac is that most damage in

Florida (with the exception of the Western Panhandle) has occurred prior to declaring Isaac a hurricane, therefore the high

hurricane deductibles will not apply to their storm related claims! This allows property owners to pay lower deductibles and

get the much needed help and relief. With the help of this blog, please stay informed of all

news pertaining to property damage and insurance claims if you own or rent a home or a business office. Keep safe and do contact me if you have any questions, suggestions or comments. You may also contact my co-workers at Zevuloni & Associates Public Adjusters who have been helping property owners with storm related claims since 2005 and are experts in the field.

Tropical Storm Isaac & Hurricane

Isaac - The Aftermath  [Wed, September 05, 2012] As insurance claims from Tropical Storm Isaac and Hurricane Isaac have

started to come in, EQECAT estimates Isaac’s insured damages in the U.S. as between

$500 million and $1.5 billion. Other sources within the insurance industry assess the losses from Hurricane Isaac to over

$2 billion. Hurricane Isaac caused severe damage along the northern Gulf Coast of the United States

in late August 2012. Isaac reached hurricane strength the morning of August 28. At least 9 fatalities have been confirmed in the United States—5 in Louisiana and two each in Mississippi

and Florida. Widespread wind, water and flood damage along the Mississippi, Louisiana and Alabama coast, as well as severe

flooding in South Florida has impacted many residential and commercial property owners. According to InsuranceJournal, "State Farm Insurance Cos., the largest insurer in Louisiana and Mississippi, said it had received

4,266 homeowners’ insurance claims in the two states — 3,805 in Louisiana and 461 in Mississippi. The company

had received 1,144 automobile claims — 998 in Louisiana and 146 in Mississippi. Allstate Corp., which is the second

largest insurer in Louisiana and third largest in Mississippi, declined to release the number of claims it has received so

far." Most of the damage from Isaac was flood

and water damage - caused by the heavy rains and storm surge which reached up to 9 feet in some areas of New Orleans. What

is the difference between flood and water damage? In general, wind-driven rain and water that comes into your home through

the roof, windows, doors or holes in the walls is water damage and is covered by homeowners insurance. However, water damage

from the bottom up -- such as the overflow of a body of water or damages caused by a storm surge (flood) – is most likely

not covered – as you may need separate flood insurance coverage for that. If you aren’t sure whether the damage is covered under your policy, contact your insurer or call a licensed

Public Adjuster to assess the damage and review your policy. The

expert team of Public Adjusters at Zevuloni & Associates are licensed in the states of FL, TX, GA, SC, NC, MD, CT, RI and

ME and have vast storm experience with assisting policyholders through Katrina, Rita and Wilma. Stay safe, educated

and prepared when it comes to storms and insurance claims.

Are You Ready?

[Fri, August 24, 2012] Hurricane Isaac, currently a tropical storm brewing southeast

of Puerto Rico, is fore-casted to approach Florida on Monday as a Category 1 hurricane. Some computer models show it may swing

further west into the Gulf of Mexico. At the time of this posting, the Sun Sentinel reported that Tropical Storm Isaac’s threat to Florida is reduced but not eliminated. [Fri, August 24, 2012] Hurricane Isaac, currently a tropical storm brewing southeast

of Puerto Rico, is fore-casted to approach Florida on Monday as a Category 1 hurricane. Some computer models show it may swing

further west into the Gulf of Mexico. At the time of this posting, the Sun Sentinel reported that Tropical Storm Isaac’s threat to Florida is reduced but not eliminated.

Regardless of the path Isaac may take, my colleagues at Zevuloni & Associates, Public Adjusters urge everyone within the cone of the storm to prepare. If you have not developed your hurricane plan and have not gotten

your supplies yet, there is still time. What you don’t want to do is wait until the last minute. Please PURCHASE hurricane supplies and PREPARE an evacuation plan just in case. REVIEW your insurance policy,

DOCUMENT the current condition of your home and business with photos, and take PROTECTIVE measures to SAFEGUARD your family,

pets and property! Prepare for the worst and hope for the best! As the

20 year anniversary of Hurricane Andrew that devastated Florida on August 24, 1992 looms within our memories, Floridians should

be extra diligent and particularly alert this time around. Please

keep my phone number nearby in case your home or business sustains any type of damage or you have a question regarding insurance

coverage or claim handling process: local: 954-742-8248; toll-free: 877.ZEVULONI (938.8566).

Below are useful links to several excellent and relevant guides

full of tips, suggestions and hurricane preparedness information.

Fri, August 24, 2012 | link

Florida Regulators Question Insurance Rate

Increases

[Thu, August 16, 2012] Florida regulators are skeptically looking into the latest increases

sought by two property insurers that could raise premiums for some Floridians by over 40 percent, even as they reduce their

number of policies. [Thu, August 16, 2012] Florida regulators are skeptically looking into the latest increases

sought by two property insurers that could raise premiums for some Floridians by over 40 percent, even as they reduce their

number of policies.

Based on the recent news reports, Castle Key Indemnity Co. (formerly Allstate Floridian Indemnity Company) and

Castle Key Insurance Co. (formerly Allstate Floridian Insurance Company) requested statewide average rate increases

of 21.9 percent and 32.4 percent, respectively, for all policy types. Company officials said they had a combined loss in surplus

from $206.7 million in 2007 to $117.5 million in 2011. David Border, vice president and state manager of the insurers, said

the increases are needed due to significant underwriting losses that have drained the insurers’ surplus. In Florida, the combined Allstate units held the No. 4 market share with more than 250,000 customers at the end of the first quarter. The company says that

number is fewer than 240,000 now. State-run insurer Citizens ranks No. 1 with 1.4 million policies, followed by Universal Property & Casualty with 567,000 and State Farm with 466,797. Regulators pressed Allstate for more information to

justify expenses related to such things as transactions with the parent company, marketing and advertising and potential storm

losses when it is not writing new property insurance business in Florida and has not been renewing tens of thousands of customers.

The company said it would respond in less than three weeks. Regulators will begin to arrive at a decision on the rate request

after that information is collected. In Palm Beach County, the average

premium would raise by 33.9 percent to $1,421 for Castle Key Insurance and by 23.5 percent to $1,049 for sister firm Castle

Key Indemnity Co. “We’ve had a net decline over five years

and that is highlighted by low storm action with no major events at that time,” said Border. What are your views

on the constant rate increases? I would greatly appreciate your feedback, questions and opinion, so please don't hesitate

to contact me.

Thu, August 16, 2012 | link

A Florida Disaster In The Making?

[Fri, July 27, 2012] Did you know that water damage is the most common loss reported

by homeowners? If you ever had significant water damage from a leak, you know that the consequences may be anything but simple. [Fri, July 27, 2012] Did you know that water damage is the most common loss reported

by homeowners? If you ever had significant water damage from a leak, you know that the consequences may be anything but simple.

Wood flooring buckles up, furniture or cabinets are soaked, carpet

and baseboards are ruined. Sometimes you may need to remove drywall and if the leak impacted electrical lines – expect

an expensive repair bill, not to mention the cost of water removal and restoration services that may run you thousands of

dollars. Well, if you think that your insurance company will cover

the costs of the loss, think again, especially if your home is insured by Citizens Property Insurance Corp. Florida’s largest state-backed property insurer is looking to reduce its coverage - such as capping

losses due to water damage to $15,000! This is a ridiculously low and incredibly inadequate amount that might cover

only a small fraction of the repair bill, replacement materials, mitigation and or rebuilding costs, making the homeowner

pay for everything else. About 35% of Citizens' water damage claims exceed $15,000

...although I suspect that many such claims have been grossly underpaid. Homeowners will end up paying out of pocket to repair

damage from everyday perils such as an air condition leak, pipe burst, faulty plumbing and a leaky roof if this policy is

catastrophically approved by the full board next week. If Citizens

proceed with this $15,000 cap on water damage claims, along with other proposed reductions and rate hikes, I foresee a disaster

in the making for thousands of Floridians already struggling financially. At a time when private insurers have not jumped

back into the market to write new homeowners policies, unfortunately many Floridians have no choice but to accept whatever

Citizens offers and hope for the best. I strongly encourage all Floridians

to contact Citizens and the local legislators to voice their concerns regarding the proposed policy limits and rate hikes.

Take a close look at your current homeowner policies to check on coverage and claims procedures. Ask contractors and plumbing

professionals how much typical repairs may cost. You are welcome to contact me if you have any questions regarding your policy coverage or a property damage claim. It is better to have all the information

at hand before disaster strikes and be prepared.

Fri, July 27, 2012 | link

Live On The Air With Cindy Graves  [Mon, July 16, 2012] Last week, I have been humbled and honored to be a guest on the

Cindy Graves Show, AM 600 WBOB in Jacksonville, Florida (www.600wbob.com). The fifteen minute live segment presented a perfect opportunity to discuss the claim process for residential and commercial

damage caused to properties in Jacksonville, FL by Tropical Storm Debby. The host – Cindy Graves, a charismatic, knowledgeable

and outspoken president of the Florida Federation of Republican Women and the State Committeewoman of Duval County, FL wasted

no time and went straight to the point. [Mon, July 16, 2012] Last week, I have been humbled and honored to be a guest on the

Cindy Graves Show, AM 600 WBOB in Jacksonville, Florida (www.600wbob.com). The fifteen minute live segment presented a perfect opportunity to discuss the claim process for residential and commercial

damage caused to properties in Jacksonville, FL by Tropical Storm Debby. The host – Cindy Graves, a charismatic, knowledgeable

and outspoken president of the Florida Federation of Republican Women and the State Committeewoman of Duval County, FL wasted

no time and went straight to the point.

Happy to be a part of the show and offer help, I covered

several important points and answered Cindy’s questions about the role of a Public Adjuster and that of a Company Adjusters.

However, fifteen minutes was nowhere nearly enough to cover all the points which I knew would be useful to property owners.

I invite you to listen to the interview part of the show and let me know what you think. Your questions, stories and suggestions are always welcome. Stay safe and

informed! Take a listen: http://youtu.be/TcsFRLfZ3mE

Mon, July 16, 2012 | link

A 48-hour Moratorium On Public Adjusters

Was Ruled UNCONSTITUTIONAL!  [Fri, July 06, 2012] A 2008 Florida law establishing a

48-hour moratorium on public adjusters was ruled unconstitutional on Thursday, July 5, 2012 by the Florida Supreme Court on

grounds that it restricted commercial speech.' [Fri, July 06, 2012] A 2008 Florida law establishing a

48-hour moratorium on public adjusters was ruled unconstitutional on Thursday, July 5, 2012 by the Florida Supreme Court on

grounds that it restricted commercial speech.'

“We

affirm the 1st District‘s decision that the statute unconstitutionally restricts the commercial speech of public adjusters

because it is not narrowly tailored to serve the state‘s interests in ensuring ethical conduct by public adjusters and

protecting homeowners,” the Florida Supreme Court justices ruled Thursday in Jeffrey Atwater v. Frederick Kortum.

The 48-hour restriction

was unjust to both the property owner and the Public Adjuster. Policy holders are typically not familiar with the details

of their insurance policies, and can make irreversible mistakes during the first 48 hours following a loss. Licensed Public Adjusters can help them get the benefits they are owed and assist them in every aspect of their insurance claim process. “Thanks

to this ruling, we can help more policyholders in those critical first hours when they need it most,” said Florida

Association of Public Insurance Adjusters' president Harvey Wolfman. “FAPIA and its

nearly 400 member public adjusters are committed to helping policyholders receive full and fair compensation following damage

to their property,” continued Mr. Wolfman. Julie Patel of the Sun Sentinel reports that "The 2008 law was enacted to prevent public adjusters, hired by policyholders

to represent them during the claims process, from contacting people when they’re in shock and haven’t had a chance

to resolve a claim with their insurer". However, I think that this is exactly when

a property owner may need the assistance of an expert working in the best interest of the insured - not the insurance company.

The first 48 hours following any type of damage - be it hurricane damage, fire,

theft, vandalism, flood, collapse, tornado damage, roof leak, sinkhole or any other insured peril is a critical

time when a property owner can greatly benefit from the knowledge, experience and guidance of a licensed Public Adjuster. I'd like to hear your views on the ruling and would appreciate any personal accounts or stories related to the subject at hand. Please don't hesitate to contact me

via email or at the office at 954-742-8248.

Fri, July 6, 2012 | link

How Can I help You? Have A Question, Just

Ask!  [Mon, June 11, 2012] Over the years I’ve gotten

a firsthand look at all the possible things that can go wrong at homes, business offices, hotels, warehouses, boat marinas

- from catastrophic events like major storms to more common problems, like kitchen fires, roof leaks, burglaries and plumbing

leaks. [Mon, June 11, 2012] Over the years I’ve gotten

a firsthand look at all the possible things that can go wrong at homes, business offices, hotels, warehouses, boat marinas

- from catastrophic events like major storms to more common problems, like kitchen fires, roof leaks, burglaries and plumbing

leaks.

Since

2005 I’ve been working with property owners and their insurance companies to ensure that claims get fairly assessed

and are justly paid so that policyholders can rebuild and move on. I work on behalf of policyholders to help people get all

that they're entitled to from insurance claims. Licensed by the State Dept. of Insurance, Public Adjusters evaluate damage and rebuilding costs,

track the flow of insurance payments and amounts due, and work with home insurance companies to expedite their clients' insurance

claims. It's better to hire a public adjuster early in the process in order to streamline your claim, since it may be more

difficult for an adjuster to come in halfway or at the end of a claim and try to work backwards to assess the situation. Understand that your insurance company

may be far more concerned with minimizing potential losses and protecting their bottom line while you simply want to restore

your business or home. Will the settlement cover your losses? Will you have to settle for substandard repairs or replacements? Will you

have to do without the quality items you lost due to property damage? Does the settlement take into account all of your losses?

Are you getting compensated for everything that you are entitled to? The average homeowner rarely files an insurance claim, making it difficult

to judge a good settlement from a poor one. Rather than taking your insurance company's representative's word for it, let

a Public Adjuster review your situation. I can help you navigate the complexities of filing an insurance claim – and

help you receive a fair and equitable insurance settlement. I can also review your policy, making it possible for you to get

an objective opinion about the worthiness of the insurance settlement offer with no obligation whatsoever. I understand the way insurance works as

well as how to spot underestimations and oversights – all of which can dramatically affect your final offer. Let me

put my expertise to work for you. The office of Zevuloni & Associates succeeds only when we can help our clients. Let me know how I can be of help. Have a question, just ask me!

Mon, June 11, 2012 | link

Your Homeowners Insurance Policy: Are You

Prepared For The 2012 Hurricane Season? [Mon, June 04, 2012] U.S. Department of Homeland Security

Secretary Janet Napolitano wants to make sure Americans are prepared for the start of the 2012 Atlantic hurricane season. [Mon, June 04, 2012] U.S. Department of Homeland Security

Secretary Janet Napolitano wants to make sure Americans are prepared for the start of the 2012 Atlantic hurricane season.

The season officially

began June 1st, and Napolitano will join Federal Emergency Management Agency head Craig Fugate, as well as Florida Gov. Rick

Scott to urge those likely to be affected by storms to prepare beforehand. Already two named tropical storms have swept through

the Southeast and caused windstorm and flood damage. As local county emergency personnel prepare for the season ahead, you

should be prepared at home as well. Two keys to weather safety are to prepare for the risks and to act on those preparations

when alerted by emergency officials. With the threat of a hurricane or major storm never far from people’s minds, insurance

is a big deal in the Sunshine State. Because of its geography, Florida is considered the most hurricane-prone state in the nation. One study says 8 of

the 10 most expensive hurricanes ever to make landfall in the United States effected Florida the hardest. Today, I'd like to explore how you can

get prepared in terms of insurance. I suggest that you: - Thoroughly review your property insurance policy. If anything is unclear or confusing, speak

with your insurance agent or a licensed Public Adjuster and get answers in a non-insurance legalese.

- Take a complete inventory of your possessions. Keep one copy in your home and the other in

another location. Take photos and keep receipts. Photo documentation will help with the claims process and can assist your

Public Adjuster in the investigation.

- Make sure that you are insured 100 percent in replacement value. Keep in mind that with the unstable real estate

sector, market value has dropped, but replacement value still remains fairly steady. Get a good idea of what your average

replacement value is per square foot.

- Know what your deductible or out-of-pocket expenses are if your property is damaged. Many

insurance companies assess a deductible that is a percentage of the policy limit, such as 2 percent, 3 percent or 5 percent.

-

Individuals who rent a house or apartment may want to look into purchasing a renters insurance policy to protect their possessions.

- Make

necessary repairs to your roof, windows and sliding glass doors.

- Trim those overgrown, dead or weak tree branches and keep your hurricane

shutters handy.

Be prepared to file an insurance claim if your property sustains damage. Keep the number of a licensed Public Adjuster handy to immediately assess the damage and guide you through the process of filling an insurance claim. Please don't hesitate

to contact me with any questions, suggestions or help. Stay safe!

Mon, June 4, 2012 | link

Vacant Home Dangers [Fri, May 25, 2012] Real estate sales have been sluggishly

growing while the number of foreclosure filings in April fell to the lowest monthly total since July 2007, according to RealtyTrac’s most recent report, released Thursday. Despite these optimistic statistics, there are many homes that stand empty—awaiting

to be sold or rented. [Fri, May 25, 2012] Real estate sales have been sluggishly

growing while the number of foreclosure filings in April fell to the lowest monthly total since July 2007, according to RealtyTrac’s most recent report, released Thursday. Despite these optimistic statistics, there are many homes that stand empty—awaiting

to be sold or rented.

This week I’d like the blog to focus on whether or not a generally insured peril will be covered by a standard

homeowner’s policy if the home is vacant. A vacant home is a property that’s

entirely empty (for a specific amount of time), without any personal property inside. For instance, an investment property was purchased

but stood vacant for several years as it was never rented or occupied. However, the property was still covered by an insurance

policy. What happens if an exterior AC unit is stolen? Does the insurance company reimburse the owner for this loss?

Based on a typical policy, the

loss would most likely not be covered because the home was never occupied. Whenever a home is empty,

the property is at a higher risk for damage. In this scenario, the carrier possibly covered this policy based on an assumption

that the property will be rented out shortly and had no documentation from the owner which stated otherwise.

Most insurance companies require either an endorsement or a separate, home insurance policy for a vacant dwelling

while the owners try to rent or sell it. Not all companies offer vacant-home policies, but some do. Such policies may have

certain restrictions or higher premiums. If a home is vacant, damage can occur and become worse over time. Because the damage

can be more expensive to fix, the premium on vacant home insurance coverage is typically higher. Insurance companies hate vacant houses, whether you’re taking an

extended vacation or you’re waiting to sell your house, leaving it empty. If you’re not home and a water pipe

busts, a fire starts, or someone breaks in, chances are the subsequent mess is going to be pretty big — along with the

insurance claim for the damage. Read the fine print in your

home owners policy to see its terms about vacancies. Then, email your agent or insurance company to double-check the rules.

Don’t call, because an email is a written record of your communication. You might need that record later if the company

refuses to pay a claim because your house was vacant. Let me know if I can be of help!

Fri, May 25, 2012 | link

Flood Damage Vs. Water Damage. Know The Difference? [Fri, May 18, 2012] “May you always have walls

for the winds, a roof for the rain, tea beside the fire, laughter to cheer you, those you love near you and all your heart

might desire.” ~Irish Blessings [Fri, May 18, 2012] “May you always have walls

for the winds, a roof for the rain, tea beside the fire, laughter to cheer you, those you love near you and all your heart

might desire.” ~Irish Blessings

As I type this, heavy rain drops cover the windows completely. With dismay, many property

owners may discover that their homes sustained unwelcome property damage such as a roof or window leak, flooded basement or

a collapsed wall. Will their insurance policy cover the damage? Will their settlement be enough to repair or rebuild? Many

homeowners dread these questions, so here are a few basic answers. Please note that each situation is different, so don't

hesitate and contact me with your questions. That depends on the type of insurance they chose, how the water entered their properties and as you know by now,

how their claim has been filed. There basically are two insurance policies that deal with a homeowner's water damage - a flood insurance policy and a homeowners insurance policy. Losses not covered

by one of these policies may be covered by the other. Knowing the losses to which your home could be exposed will help you

decide whether to buy one or both of this insurance coverage.All policies have their own provisions,omissions and clauses

that you should be familiar with.

While insurance policies may differ in the coverage provided, there often are basic features common to all policies.

Ask your insurance agent or a licensed Public Adjuster about the specifics of your insurance policy and the needs based on

your location. In the meantime, here’s general information based on a typical insurance policy. FLOOD INSURANCE. As the name implies, a

standard flood insurance policy, which is written by the National Flood Insurance Program, provides coverage up to the policy

limit for damage caused by flood. The dictionary defines "flood" as a rising and overflowing of a body of water

onto normally dry land. For insurance purposes, the word "rising" in this definition is the key to distinguishing

flood damage from water damage. Generally, damage caused by water that has been on the ground at some point before damaging

your home is considered to be flood damage. A handful of examples of flood damage include: A heavy rain seeps into your basement because the soil can't absorb

the water quickly enough A heavy rain or flash flood causes the hill behind your house to collapse into a mud slide that oozes into your

home. Flood damage to your home can be insured only with a flood insurance policy - no other insurance will cover

flood damage. Flood insurance is available through your insurance agent, insurance company or local Federal Emergency Management

Office (FEMA). To determine if your home is located in a flood plain, contact your county planning office. If you are living

in a flood plain, flood insurance may be an excellent purchase. HOMEOWNERS INSURANCE. A homeowner’s insurance

policy doesn't provide coverage for flood damage, but it does provide coverage for many types of water damage to your home.

Just the opposite from flood damage, for insurance purposes, water damage is considered to occur when water damages your home

before the water comes in contact with the ground. A few examples of water damage include: A hailstorm smashes your

window, permitting hail and rain free access into your home. A heavy rain soaks through the roof, allowing water

to drip through your attic or ceiling. A broken water pipe spews water into your home. Even if flood or water

damage is not covered by your homeowner’s insurance policy, losses from theft, fire or explosion resulting from water

damage is covered. For example, if a nearby creek overflows and floods your home, and looters steal some of your furnishings

after you evacuate, the theft would be covered by your homeowners insurance because it is a direct result of the water damage.

However, the flood damage would be covered only if you have flood insurance. It's important to note that flood insurance

and homeowners insurance do not duplicate coverage for water damage. Instead, they complement each other. Do your research,

ask me questions about any water damage sustained to your property and stay safe!

Fri, May 18, 2012 | link

The Mostly Useless Perils Homeowners Insurance

DOES Cover [Thu, May 03, 2012] Volcanoes and Spacecraft? Do you know

what your homeowners insurance policy covers? Most people have a general idea, but do not invest the time to thoroughly read

all the details, exclusions and the fine print of their policies. However, if you do decide to flip through the pages you

might be surprised to learn about some of the things your policy actually does cover. Whether or not you need this coverage

or lack coverage that is vital based on your location and climate - is a different discussion which I will gladly participate

in if you contact me. [Thu, May 03, 2012] Volcanoes and Spacecraft? Do you know

what your homeowners insurance policy covers? Most people have a general idea, but do not invest the time to thoroughly read

all the details, exclusions and the fine print of their policies. However, if you do decide to flip through the pages you

might be surprised to learn about some of the things your policy actually does cover. Whether or not you need this coverage

or lack coverage that is vital based on your location and climate - is a different discussion which I will gladly participate

in if you contact me.

The focus

of this blog entry is to let you know of a few rather rare things that most policies cover that you would probably never think

to ask about. (Please note that all policies differ and you should consult your insurance agent and provider for specifics

on your coverage).

Volcanic Eruptions – although the majority of homeowners don’t live close enough to an active

volcano to worry about, if you did - it’s good to know you’d be covered! Most homeowner’s policies provide

coverage for property loss caused by volcanic eruption when it is the result of a volcanic blast, airborne shock waves, ash,

dust, or lava flow. It is important to note that damage to land, trees, shrubs, lawns, property in the open, open sheds,

or the contents of those open sheds are typically not covered. Neither is the cost to remove ash from personal property is

generally not covered unless the ash first causes direct physical loss to personal property. Aircraft & Spacecraft Damage

– damage to property inside the building

would be covered if the falling debris first damages and penetrates the building roof or walls, then damages the property

on the inside. Some insurance policies include the terms "falling objects" and "aircraft," which include

self-propelled missiles (meteors) and spacecraft. State Farm states on their website that while claims are handled on a case-by-case

basis, damage from satellite debris, a.k.a. space junk, likely would be covered under most insurance policies. Hopefully your home will not be damaged

by a volcano or an aircraft, but at least you know you are covered …well, sort of. When shopping for insurance, it is important to understand

exactly what you are getting and what you are lacking in a homeowner policy. As I have previously written, when it comes to

insurance – the devil is in the details. Do your homework and research. Get a free evaluation and analysis of your policy from a licensed Public Adjuster. Although Public Adjuster don’t sell insurance, nor do they get any commissions from the sales, they know which coverage

is vital and which can be tossed. Their knowledge comes from the numerous experience of handling property damage claims in

your area of residence and dealing with insurance companies. Stay safe and do ask questions, I am here to help!

Thu, May 3, 2012 | link

Angry Homeowners To Citizens: We Are Paying

More But Getting Less ... [Wed, April 25, 2012] Dave Berman of Florida Today wrote a stimulating article regarding a recent meeting of 330 concerned residents in Barefoot Bay, FL on April 24th, 2012

to complain about insurance coverage on their manufactured homes. [Wed, April 25, 2012] Dave Berman of Florida Today wrote a stimulating article regarding a recent meeting of 330 concerned residents in Barefoot Bay, FL on April 24th, 2012

to complain about insurance coverage on their manufactured homes.

The outraged homeowners packed a community center meeting room to express

their views on the latest rate hikes and the unjust changes to their policies. The meeting was a bit heated at times, and

at least some in the audience left the meeting unsatisfied. One of the immediate concerns at Barefoot Bay is the decision by Citizens to discontinue offering

insurance coverage for carports and pool and porch screens, effective when policies are renewed this year. At the same time,

Barefoot Bay homeowners are seeing their Citizens premiums rise by an average of 10 percent this year. According to the article,

Barefoot Bay residents typically pay Citizens $1,500 to $2,600 a year to insure their manufactured homes. Citizens Property Insurance Corp is the

state's largest property insurer with over 1.4 million customers. It was created to provide hurricane coverage to property

owners who could not get insurance from private carriers and lately it has been increasing rates while reducing coverage.

Anyone who

owns a house in Florida knows that property insurance has continued to rise, even without any major catastrophes in the past

seven years. Rates in Florida will now be more dependent on the insurance market, and if they happen to balloon, there isn't

much regulators can do about it. The state's catastrophe fund sells insurance to insurance companies. Right now it only has

enough cash on hand to cover one big storm over a 20-year period. Citizens was supposed to be the insurer of last resort in Florida, but

ended up with a larger pool than expected. Citizens reported that its policy count is continuing to decline. As of March 31,

Citizens had 1.44 million policies, down 2.4% from the end of January – while total risk fell 10% over that period to

$503 billion. The reduction is due to private insurers removing policies, primarily from Citizens’ residential multi-peril

and wind-only books of business. Citizens’ board also moved in February to reduce coverage for secondary structures, personal contents, new

construction and personal liability, as well as to increase sinkhole deductibles by 10%. As of May 1, Citizens is refusing

to insure properties valued at more than 1 million. Also no longer covered this year are most porches, decks and outbuildings.

I applaud the

residents of Barefoot Bay for voicing their concerns and standing up to Citizens. I also hope that in case of any damage sustained

to their homes they will elect to call an experienced and licensed Public Adjuster to ensure that they will get a maximum

settlement allowed by Citizens to fix or rebuild their homes. I would love to get your thoughts and comments on this issue, and have you participate in

the blog. Do you have a policy with Citizens? What has your experience been like? Please leave a comment below or contact

me at joe@florida-pa.com.

Wed, April 25, 2012 | link

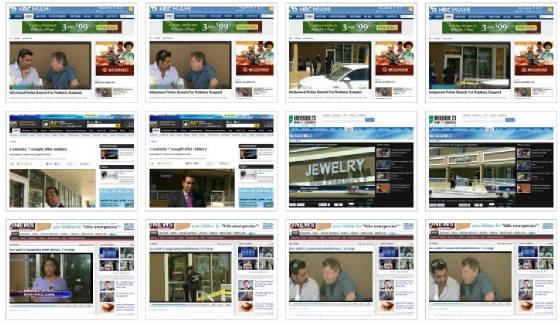

Jewelry Heist, Zevuloni & Associates

Called For Help  [Fri, April 20, 2012] No doubt about it, getting a theft

claim settled quickly & successfully with an insurance company is not a simple task. However, after adjusting many such

claims, a pattern begins to emerge. [Fri, April 20, 2012] No doubt about it, getting a theft

claim settled quickly & successfully with an insurance company is not a simple task. However, after adjusting many such

claims, a pattern begins to emerge.

To begin with, nearly all theft claims are looked at with suspicion – especially by the insurance companies.

Therefore the burden of proof, proper documentation, taking preventative measures, compliance with all requirements and clauses

of the insurance policy and fulfilling the duties right after the loss as stated in the policy are integral to a fair settlement.

Earlier this

week I was called to the scene of a jewelry store robbery. A robbery covered by the local media in the heart of a busy strip

mall in Hollywood, Florida. The Hollywood Police Department apprehended 3 suspects while the 4th one is still on the run (as

of this posting). All three had handguns and used stolen vehicles as the getaway cars. Based on recent statistics, crime against jewelry

stores and firms result in losses over $125 million annually. On the average, 10-15 homicides occur annually during jewelry

store robberies. Jewelry stores are high-profile targets for robbers. Retail jewelers are at the greatest risk. I am confident

that my involvement and expertise will give the worried and frazzled owner of the jewelry store a piece of mind, justice and

a fair insurance settlement. I welcome your comments or questions on this subject at joe@florida-pa.com. Stay safe! Below

are several photos of myself that were captured by the media at the scene of the crime.

Fri, April 20, 2012 | link

|